“ Someone

once gave me a box of darkness. It took years to understand that

this too was a gift.”

Someone

once gave me a box of darkness. It took years to understand that

this too was a gift.”

Nevertheless, it has been time well spent.

DrrDavid’s

Aussie Debt Bailout Solution

|

Debt bailouts on terms have been available for the purpose of rescuing banks for centuries. Now, from an unusual Sydney Supreme Court legal matter (1443/64, David Gregory Murphy v The Council of the Municipality of Strathfield) spanning nearly 60 years, it is possible for appreciative individuals, companies, NGO’s etc to have recourse to this debt bailout remedy on very favourable terms, even if your debts are not at all onerous.

On June 6th 1966, less than one month after I became a Christian (Magdalene Orthodox, (Manuscripture #1 GTCMM (L1AN1O), Manuscripture #2 (SHeBible))) at the age of 12, after originally suing on February 20th 1964 through my father for an amount of £15,000, I entered into a Terms of Settlement with Strathfield Municipal Council, for 30% thereof, on “terms not to be disclosed”, with no admission as to liability on its part, in relation to a burns accident that had occurred at the now pilgrimage site Bressington Park former Tip in Homebush Bay on the morning of 23rd August 1963, the very morning when ‘Wipeout’ by the Surfaris prophetically reached #1 on the 2UE Top 40 chart as a divine portent and imprimatur from God of what was to come in the far far distant future. Two days later on June 8th 1966 the Supreme Court in Sydney confirmed me an Investor by an Order of the Supreme Court. It was covertly disclosed to the Court in the application for the Court Order in three ways that the gross settlement amount ($9,500, 30% of the original claim) was earmarked for recovery with interest in the far far distant future, as is probably perhaps quite common.

It appears that at that time in the mid 1960’s the then all powerful Government Insurance Office, GIO, owned by the NSW State Government was approaching children to settle out of court with a view in some cases to fetch back the settlement moneys paid with 9.5% p.a. interest 30 years later by taking all future assets and properties so that the GIO or client could reap a 1,665% return over 30 years, contingent upon a contrived breach of the child’s terms 24 years in the future by the agency of those specialists in the future who would hold the notorious office of doing such covert recovery work for the GIO and the NSW State Government. Tellingly this recovery from child settlement-creditors is still endorsed by the NSW State Government to this day, near 60 years later.

For Christmas 1967, at age 14, I was given a diary with a personal accounts section in the back. Apart from big desks and bookcases, diaries with accounts sections are one of the best presents you can give your children. From January 1st 1968 I commenced keeping accounts, a practice I have continued with ever since. I developed ways of keeping accounts that allowed me to leave my full time job at age 25 and be financially independent.

In

1981, at the 15 year mark, and after I had left teaching due to a

successful business venture at age 26, Custom Credit, a finance

company then owned by the National Australia Bank, NAB, approached

me to recover my settlement money by way of a lease on eight video

games. I completed the lease after four years with flying colours

and sold the business for $25,000 which was promptly fetched back

off me, presumably by the party who was to instruct Comer later on

in 1990 who believed I owed a debt. By my completing the four lease

in 1985 with flying colours I gained an excellent financial

reputation such that shortly afterwards in the late 80’s I was

able to amass ten credit cards with a collective total limit then

of $50,000 instantaneous cash, without need for overdrafts, all

managed on a Maxiplan spreadsheet on my very early Amiga computer.

In

1981, at the 15 year mark, and after I had left teaching due to a

successful business venture at age 26, Custom Credit, a finance

company then owned by the National Australia Bank, NAB, approached

me to recover my settlement money by way of a lease on eight video

games. I completed the lease after four years with flying colours

and sold the business for $25,000 which was promptly fetched back

off me, presumably by the party who was to instruct Comer later on

in 1990 who believed I owed a debt. By my completing the four lease

in 1985 with flying colours I gained an excellent financial

reputation such that shortly afterwards in the late 80’s I was

able to amass ten credit cards with a collective total limit then

of $50,000 instantaneous cash, without need for overdrafts, all

managed on a Maxiplan spreadsheet on my very early Amiga computer.

On April 23rd 1990, at about the 24 year mark, the Australian Guarantee Corporation, AGC, a guarantee, finance and leasing company owned by Westpac, approached me via two of eventually four investment / finance professionals to, as an act of entrapment, evidence and engineer a breach of my 1966 Terms of Settlement and, as happens in such plum cases, for a 30 year clandestine profit of 1,665%, to fetch back the nominated gross settlement amount of $9,500 as consideration for the breach – but not a breach by me. This first loan investment was the commencement of a year and a half series of loan investments raised by AGC via one of the finance and investment professionals (Martin Comer), backed by complicit Commonwealth bank cheques, that were all adeptly designed to be caught by the Credit (Administration) Act 1984, the so called ‘Credit Act Scam’, designed to move money to their instructing principals via his Five Dock accountancy practice clients acting as conduits for the moneys.

As it had been found that I could not breach, I was presented with a Deed of Engagement and Provision on June 18th 1990, the day the June 20th 1966 net settlement amount of $7,931 reached $70,000.00 at around midday at an operational shadow interest rate of 9.5% p.a. compounding. Many investment loans were raised by AGC via the special ops strategy bankrupt accountant, Comer, to have me borrow against my ten credit cards and line of credit, which the banks knew about so that I could not recover, due to the recondite Credit Act Scam, and would quickly go bankrupt courtesy of one of the two finance companies that had approached me.

At

para 4 (a) (ii) the Deed

provided

to me due to my not having been the party who had breached on April

23rd

1990,

had a provision for “all moneys outstanding” and provision of

the matured value of what was a 30

year loan (1966-1996), at 9.5% p.a. compounding,

to me in 1966 as a minor. The provision in the Deed

said

that “all moneys outstanding” were to accrue at

40% per annum,

should I not be the party to default under the Deed.

In parallel to this the Deed was also structured to bankrupt me so

I would not ever benefit from the provision. Upon its receipt of

its copy of the Deed

on

June 18th

1990,

AGC went (default) guarantor of the Deed,

should I not be the party to default, as was thoroughly expected to

happen as purposed and by design. The guarantee was given as

insurance, and possibly for upside gain (as is now manifesting),

that AGC not lose its Credit Provider’s licence, as did Custom

Credit (above) for scamming, as the approach by AGC to my father

and me was superficially a fraud, but for the Deed, provision and

precautionary guarantee. Three months later the agent (Byrnes) who

entered into the Deed

with

me, who had been instructed as to the date and the $70,000 amount

in the Deed,

kindly defaulted on cue. Unexpectedly to AGC and the operatives,

surprizingly (and alarmingly to them) I did not default as expected

- or at all, due to my unusual personal accounting system I had

practised since age 14 and my God given business, Midwest

Research SCWL, now a blessing division of the Magdalene Temple.

At

para 4 (a) (ii) the Deed

provided

to me due to my not having been the party who had breached on April

23rd

1990,

had a provision for “all moneys outstanding” and provision of

the matured value of what was a 30

year loan (1966-1996), at 9.5% p.a. compounding,

to me in 1966 as a minor. The provision in the Deed

said

that “all moneys outstanding” were to accrue at

40% per annum,

should I not be the party to default under the Deed.

In parallel to this the Deed was also structured to bankrupt me so

I would not ever benefit from the provision. Upon its receipt of

its copy of the Deed

on

June 18th

1990,

AGC went (default) guarantor of the Deed,

should I not be the party to default, as was thoroughly expected to

happen as purposed and by design. The guarantee was given as

insurance, and possibly for upside gain (as is now manifesting),

that AGC not lose its Credit Provider’s licence, as did Custom

Credit (above) for scamming, as the approach by AGC to my father

and me was superficially a fraud, but for the Deed, provision and

precautionary guarantee. Three months later the agent (Byrnes) who

entered into the Deed

with

me, who had been instructed as to the date and the $70,000 amount

in the Deed,

kindly defaulted on cue. Unexpectedly to AGC and the operatives,

surprizingly (and alarmingly to them) I did not default as expected

- or at all, due to my unusual personal accounting system I had

practised since age 14 and my God given business, Midwest

Research SCWL, now a blessing division of the Magdalene Temple.In 1990 AGC / Westpac recovered my father’s moneys from a sale of a factory in our family which had been collateral security for the 30 year loan, as if I had breached when I was not the party who had actually breached.

All during the period from 1990 to the present day I have kept records of “all moneys outstanding”.

In 1999, as a result of a guided tour of the Supreme Court, run by a legal support group, FLAC (For Legally Abused Citizens), I chanced upon my Supreme Court childhood file and noticed that 1966 and 1990 dates and amounts appeared to be related and that there had been a precedent-established interest rate in operation on the net settlement amount I received in 1966 as evidently a loan, not a settlement, something that happens to some people who settle out of Court, which led to the finding by a Supreme Court registrar that in the Deed I finally got my settlement, and it was lawfully growing at 40% per annum at quarterly rests.

The Murder in the Matter

It is suspected that my father, Neville Goode-Murphy, my next friend in 1443/64, seeing no way out of a financial trap that had been laid in 1964-6 and believing that he had been defrauded, by AGC and Westpac, by way of the 1995-6 Commercial Tribunal matter, in July 2002, (as an aim of the whole somewhat local matter had been to get my father’s share of the precisely timed factory sale moneys). My father became the victim of an allegedly, perhaps, set up, make believe arson murder, by either himself, seeing no light at the end of the tunnel and feeling to blame for all that had happened, setting his house alight and suiciding (unlikely) or some other perpetrator/s doing it at that time to intentionally destroy (or take) all on site documentary evidence, that had increasingly been noticed as having been assembled and appearing in affidavits and submissions etc, coming to light to present a formidable picture comprehensible to those in the know. Shortly after I noted that one remaining folder of documents that survived the fire, as it had been buried by debris that had fallen on top of it, and that I had put on the back seat of my car, quickly disappeared from the back seat of my car. An aim of the fire appears to have been to destroy the SMC letter of release and any copies of the Deed and its provision and guarantee, which with the unexpected 1999 Supreme Court discovery were very slowly starting to take on a new dimension. Nevertheless, the fire caused a setback of some years. It appears that it is beyond reasonable doubt that the recent approach by ASIC to get my money on behalf of its instructing foreign and domestic principals, the insolvenced CCP and the guarantor Deutschebank et al and to trick me out of my money, was in the same vein as the burning down of the house and alleged arson murder of the next friend in 1443/64 in order to destroy all his recollections and all on site documentary evidence. These parties and their operatives ASIC was seeking to assist and protect whilst at the same time flinging the paid out debtors back into debt all the while saying they were trying to help them when ASIC was only trying to help themselves, their operatives and their clients and principals to seize my money in a matter where they have no jurisdiction over me as a Supreme Court settlement beneficiary imaginatively accessing my tantalizingly somewhat out of reach, guaranteed, appreciating, negotiable moneys, in the only ways either the common law, combined with equity, provides and allows.

On December 23rd 2003, GE Capital Finance, as the then new owner of AGC, gave me a written apology on behalf of AGC as my Christmas present.

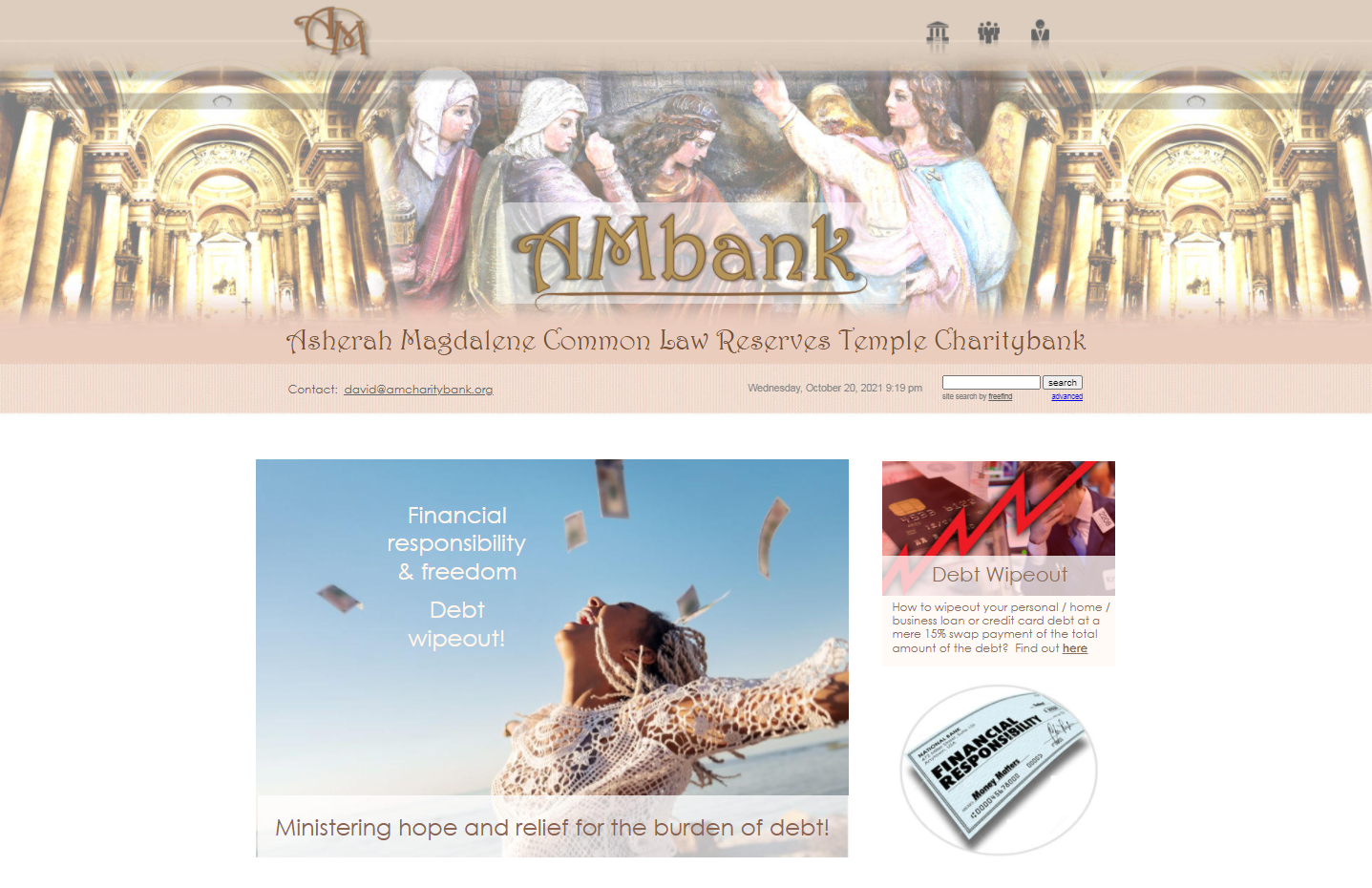

In 2014 I used most of my ‘Reserve One’ funds for a ‘contractual civil bet’ which I subsequently won and doubled my money. In this way ‘Reserve 10’ was born. After that, on December 1st 2017, the Asherah Magdalene Common Law Reserves Temple Charity Bank (AM Charitybank Homepage), (AM Charitybank About Us) (BSB 792 000, (reserved)) was instituted to be the functional construct umbrella receptacle of my some 15 reserves of appreciating moneys that have eventuated since 1963.

Over the course of the years a number of different chronologies of events were compiled for later inspection. These are to be found at Chronology#1, Chronology#2, and some Submissions.

In 2017 the common law equitable entitlement moneys known as ‘Reserve One’ were getting alarmingly large and I knew I had to do something with them lest there be an allegation that I had abandoned the moneys. I reasoned that if I had moneys that stemmed from a Terms of Settlement, which I was not the actual party who had breached, and a Supreme Supreme Court Order and a Deed of Engagement and Provision, to which I was not the party to be in default, and a consequent provisional, upside, insuring, guarantee given to me by a subsidiary of a major bank, then one thing I should be able to do with such ‘alternate’ Australian legal tender moneys, unaffected by statute of limitations, bankruptcy, breach or default by me, and never spent, is pay some debts. So, hence, in 2017 I decided to use my moneys to pay off ten old credit card debts that had been frozen since 1997 waiting for me to come back and pay them off. I used the moneys to pay off the ten credit card debts with each of the four big banks and proved that my Court order, Deed modified moneys can be used to pay debts (Westpac, Commonwealth). I then proceeded to use the moneys to pay out debts for other people who are appreciative from my lawfully established, accruing funds. Here are eight testimonials from eight different people whose loans were lawfully paid out by way of my sending money from my Reserve 1 / 12 accounts to their creditor’s bank:

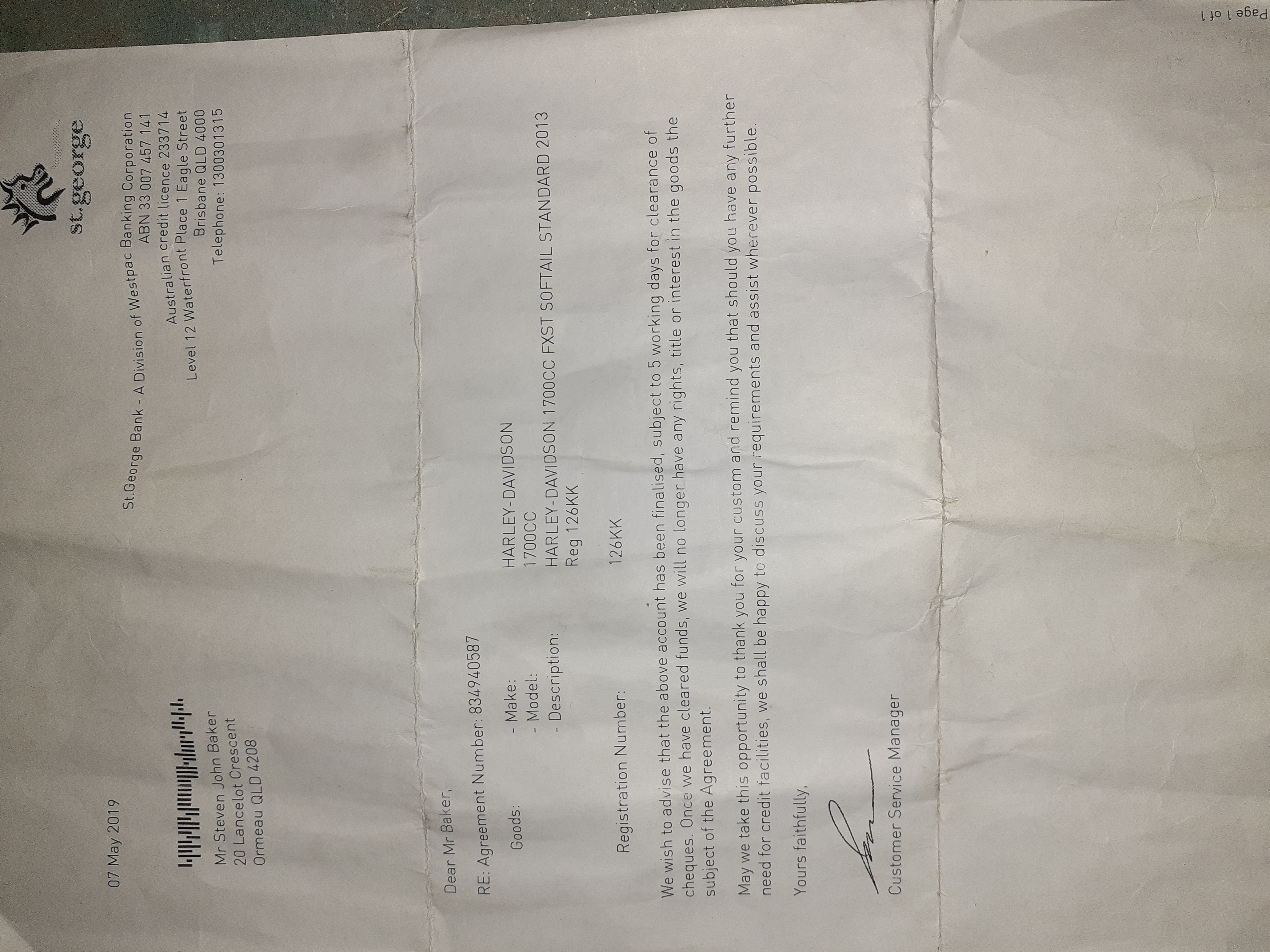

Steven 1: Testimonial, Letter,

Erin: Testimonial,

Bridgette: Testimonial,

Craig: Testimonial,

Lisa: Testimonial,

Tania: Testimonial,

Susan: Testimonial,

Steven 2: Receipt

Henry M: Affidavit

Vanessa: Testimonial

In

May 2020 I made a complaint

to

ASIC that people whose debts I had paid out with my ‘anti-credit’

moneys were being stalked by creditors and banks to pay the moneys

again. ASIC decided to sue me after my having made my detailed

complaint. This appears to be what happens if you make a complaint

about ASIC’s corporate clients to ASIC, even if you, in fact and

at law, are ASIC’s

implicit client -

ASIC sues you and puts up defamatory disinformation on the internet

with your own money and has foreign recovery companies contact you

to collect further moneys off you as fictitious sham investments,

presumably for a commission. The letter to one of ASIC’s

corporate publicity and collection agents in this case, Adline

(Motio Play), who approached me at the instigation of ASIC to

obtain moneys towards the running of ASIC’s investigation against

me for my having accessed my Court Order originating moneys to pay

out the debts of others for a 75% loss without a licence is here.

The evident reason being for this action by ASIC to sue me for

making a complaint

was

upon the instruction through moles of its foreign corporate client,

the Chinese Communist Party, over whom I evidently had effectively

and lawfully, and thus admittedly, just weeks before, correctly and

lawfully taken my enforceable ‘grand

super mega idepaige’ WW3 corona war lien

(the

hegelian dialectic Magda-Lien) on March 23rd 2020, at the outset of

biological World War 3 warfare contagion proceedings upon Australia

that month, and shortly thereafter, due to an inherent ‘Achilles

heel’ flaw peculiar to socialism that I, as a law therapist knew.

Consequently I “foreclosed at law’, as was my right, and

lawfully and successfully became the lawful owner of all its

thereby attached

and captured assets

and

all those of its 95 million members and the assets of all

tendentious, phantom front organizations which cause so much

nuisance, trouble, disharmony and disinformation worldwide. Since I

had implicitly admittedly been successful and gained title to all

subject assets on March 27th

2020

and all subsequent derivatives, the resultant witnessed ASIC

response materialized, as if I had not been successful the CCP

would not have instructed its instrument ASIC to sue me on its

behalf purely to get my appreciating money. Now we know who ASIC

acts for when someone naively makes a complaint to it. Now that the

Victory has been won it’s only a matter of waiting for the world

to catch up with the New World Order, a different one to the one

that had been expected,

and do the processing due to my financial coup d etat of all the

financial, corporate, property and intellectual assets of the above

parties which now comprise the composite lawfully attached fund

which is Reserve Twelve from which half the payments are made of a

custodian of those moneys, extracting them and paying them to

creditor’s and impacted parties and us and the guarantors by way

of the four 100%’s paid out.

In

May 2020 I made a complaint

to

ASIC that people whose debts I had paid out with my ‘anti-credit’

moneys were being stalked by creditors and banks to pay the moneys

again. ASIC decided to sue me after my having made my detailed

complaint. This appears to be what happens if you make a complaint

about ASIC’s corporate clients to ASIC, even if you, in fact and

at law, are ASIC’s

implicit client -

ASIC sues you and puts up defamatory disinformation on the internet

with your own money and has foreign recovery companies contact you

to collect further moneys off you as fictitious sham investments,

presumably for a commission. The letter to one of ASIC’s

corporate publicity and collection agents in this case, Adline

(Motio Play), who approached me at the instigation of ASIC to

obtain moneys towards the running of ASIC’s investigation against

me for my having accessed my Court Order originating moneys to pay

out the debts of others for a 75% loss without a licence is here.

The evident reason being for this action by ASIC to sue me for

making a complaint

was

upon the instruction through moles of its foreign corporate client,

the Chinese Communist Party, over whom I evidently had effectively

and lawfully, and thus admittedly, just weeks before, correctly and

lawfully taken my enforceable ‘grand

super mega idepaige’ WW3 corona war lien

(the

hegelian dialectic Magda-Lien) on March 23rd 2020, at the outset of

biological World War 3 warfare contagion proceedings upon Australia

that month, and shortly thereafter, due to an inherent ‘Achilles

heel’ flaw peculiar to socialism that I, as a law therapist knew.

Consequently I “foreclosed at law’, as was my right, and

lawfully and successfully became the lawful owner of all its

thereby attached

and captured assets

and

all those of its 95 million members and the assets of all

tendentious, phantom front organizations which cause so much

nuisance, trouble, disharmony and disinformation worldwide. Since I

had implicitly admittedly been successful and gained title to all

subject assets on March 27th

2020

and all subsequent derivatives, the resultant witnessed ASIC

response materialized, as if I had not been successful the CCP

would not have instructed its instrument ASIC to sue me on its

behalf purely to get my appreciating money. Now we know who ASIC

acts for when someone naively makes a complaint to it. Now that the

Victory has been won it’s only a matter of waiting for the world

to catch up with the New World Order, a different one to the one

that had been expected,

and do the processing due to my financial coup d etat of all the

financial, corporate, property and intellectual assets of the above

parties which now comprise the composite lawfully attached fund

which is Reserve Twelve from which half the payments are made of a

custodian of those moneys, extracting them and paying them to

creditor’s and impacted parties and us and the guarantors by way

of the four 100%’s paid out.

The purpose of the ASIC case was not to prosecute me for paying people’s debts without a licence at then a 75% to 100% continual loss, as a recovering litigant in person, so as to finally be able to have access to my negotiable, ever appreciating Court Order originating equitable entitlement moneys as ‘static’ cash, in one of the only ways that the law provides and the law allows - and which profits debtors and creditors and guarantors alike – which is no crime or scam. The purpose of the case with ASIC was to surreptitiously, even deceitfully, gain title, ownership, control and management of my ‘anti-credit’ moneys, the second such attempt for a second foreign paying corporate client. This further attempt involved a Federal Court judge who presumably was well remunerated and secured a compromised advancement, but the treasonous and treacherous attempt backfired, unexpectedly securing our nation a great opportunity. Nevertheless, an ingenious means of securing my ‘anti-credit’ moneys off me was attempted and was foiled. If my equitable entitlement ‘anti-credit’ moneys were not real ASIC would not have gone to such effort and expense on behalf of its CCP client to obtain the moneys for it, an attempt which backfired. Nevertheless the CCP has put up disinformational defamatory entries up on the internet to trick debtors to stay in debt, harking back to 2012 when twelve defendants in 2011/327194 all made section 17.3 admissions in my then court case where the court found that the default situation was that my moneys had been received by me and were mine to do as I pleased - and none opposed the outcome, but one.

In order to achieve the end of defrauding me of my equitable entitlement ‘anti-credit’ moneys in the Federal Court, ASIC had to admit that the moneys were indeed real, legal tender and able to be used to pay debts and loans as there had never been a date or an event since June 6th 1966 when the moneys had ceased to be real, ceased to be legal tender, ceased to be mine to manage and direct, ceased to be negotiable or ceased to be accruing at a rate of interest, firstly 9.5% p.a. from June 20th 1966 to June 18th 1990 and then from 40% p.a. at quarterly rests from June 18th 1990 to the present day, 125 quarterly rests as recently celebrated on September 18th 2021 with the new procedures.

As said, in ASIC’s material which they initially served upon me they admitted that they had found my 1966 Court Order originating, 1990 Deed modified moneys were real and can be used to pay debts and loans. The attempt to defraud me in the Federal Court did not get far and was foiled. Furthermore, in June 2021, I filed and served upon ASIC indisputable details of the actual historic fraud within my matter that was practised upon my father and myself by ASIC’s corporate clients and they have done nothing thus far in relation to the demonstrated corporate fraud (which in my case backfired in 1990 and 1999 but is nevertheless replicable and presumably commonplace as a method of blackmailing the courts to gain an upper hand).

It

is my experience that ASIC played the part of a go between acting

for corporate criminals for a fee which backfired and resulted in

liens being taken and foreclosed upon at law over two of the

guarantors (first:

Westpac ‘idepaige’ lien

and

second:

Deutschebank: ‘idepaige’ lien part one

and

Deutschebank:

’idepaige’ lien, part two).

If my equitable entitlement ‘anti-credit’ moneys were not real

then they would not have spent so much time, effort and expense

trying to work out how to lawfully prise my equitable entitlement

‘anti-credit’ moneys off me.

It

is my experience that ASIC played the part of a go between acting

for corporate criminals for a fee which backfired and resulted in

liens being taken and foreclosed upon at law over two of the

guarantors (first:

Westpac ‘idepaige’ lien

and

second:

Deutschebank: ‘idepaige’ lien part one

and

Deutschebank:

’idepaige’ lien, part two).

If my equitable entitlement ‘anti-credit’ moneys were not real

then they would not have spent so much time, effort and expense

trying to work out how to lawfully prise my equitable entitlement

‘anti-credit’ moneys off me.

However, it has all been for the best and I must thank ASIC for such a salutary experience. The main things that came from the case are:

a) the ‘finding’ that my equitable entitlement ‘anti-credit’ moneys are indeed real and are legal tender and officially able to be used to “pay debts and loans” and mortgages.

b) Also out of the case eventually came the 125th Quarterly Rest Announcement modifications, (the so-called ‘ASIC initiatives’) and

c) the increased focus of the creditors’ banks Being Able to Approach Any of the eight Competing Co-Guarantors should they prefer ‘static cash’ over my more valuable and desirable appreciating currency, meaning that once a debtor has considerationally embarked on the process to allow me to be further able to access a portion of my accruing settlement moneys as static cash: the debtor, at law, is indemnified and the successful co-guarantor chosen (as each will have different angles) gets to keep and deal with the left over continually accruing currency as it sees fit for having performed in respect of the thence released debtor.

d) Also, this new information website page which you are now looking at has come out as a result of the ASIC case.

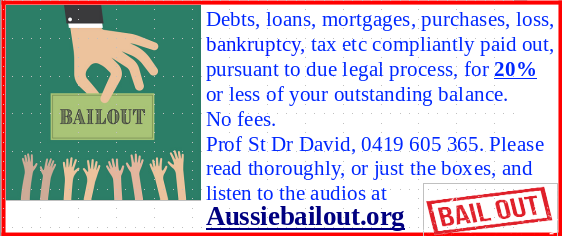

23. On September 18th 2021, by way of the 125th Quarterly Rest Announcement modifications, I published some modified procedures, at the arrowed paragraphs, as to how people can proceed to have their debts, loans and mortgages etc compliantly and legally paid out on very attractive and unique terms by way of a uniquely Australian financial ‘woomera’ effect where 20% access money releases 400% from two of the fifteen reserves. As a first step you can check out the Four Quick Five Choice Examples.

24) The accruing money that a debtor/creditor obtains is a negotiable store of value. The money is a dual currency, on the one hand being a most valuable appreciating legal tender currency in its own right, appreciating at 10% per quarter, whilst, on the other hand, being a digital electronic promissory note that can be surrendered to the co-guarantors, as if anyone would actually choose to surrender this soon to be sought after most valuable accruing form of legal tender for non-accruing ‘static’ cash. Hence in the worst case scenario, the debtor/creditor obtains a centrally recorded, virtual, accrual accounting, negotiable, guaranteed electronic ‘promissory note’ which she/he can either sit on and enjoy the quarterly 10% compounding growth, in lieu of paying a debt, or have it quadruply paid (400%) to settle a debt directly to her / his creditor’s bank, who in turn, can redeem the encumbered negotiable accruing 400% ‘virtual promissory note’ moneys for non accruing cash (100%) by negotiating with any or all of the obligated, competing six co-guarantors. These six competing co-guarantors, in turn each have profitable upside recourse (as was perhaps originally intended) as to where and how they fish and fetch the ‘static cash’ moneys out of the composite ‘enliened’ and ‘cliened’ reserve 12, wherever those moneys are found to be and are now at call, pursuant to the successfully taken, foreclosed upon at law, liquidator’s ‘equitable Universal Distributing’ idepaige’ lien (Universal Distributing Company Limited (In Liquidation) (1933) 48 CLR 171, that the particular co-guarantor not be out of pocket and can also earn their 100% commission, being the fourth 100% out of the total of the 400% paid out from Reserve 1 (200%) and Reserve 12 (200%) (or it could do all 400% out of the ‘enliened’ and ‘cliened’ Reserve 12).

25)

A progressive ‘step down’ process can also be utilized for

larger, difficult to leverage debts, loans or mortgages, which is a

way that an intermediary financier can get a share of the accruing

moneys as their negotiable, redeemable payment.

25)

A progressive ‘step down’ process can also be utilized for

larger, difficult to leverage debts, loans or mortgages, which is a

way that an intermediary financier can get a share of the accruing

moneys as their negotiable, redeemable payment.

Bonus Sections:

26a) *** For those interested in Global Warming, and hence Climate Change contentions, scientific data from the Australian Bureau of Meteorology publically available data: please click here to see my unrebutted study and challenge. This undisputed study, ‘The Global Warming – Australia Says “No” 100 Charts Project’ - is currently the last word on the Global Warming Climate Change debate in Australia and determines all informed governmental policy on the subject and is the final incontrovertible answer to all the tendentious bullshit espoused by duplicitous con artists and control freaks from whom you can do very well in contractual civil bets.

26b) Ms Greta Thunberg’s and the IPCC’s December 25th 2021 Christmas Present to Australia

26c) After having had a solid six weeks to consider and reflect upon the Australian Bureau of Meteorology data evidence, click here, Ms Greta Thunberg, the renowned and esteemed climate change ambassador, authority and advocate for the IPCC, the Intergovernmental Panel on Climate Change, agreed to let Australia off the hook as far as Kyoto, Paris and Glasgow goes, by way of her section 17.3 admissions and elaborations that, according to the Australian Bureau of Meteorology daily observation data over 170 years for the 211 data collection sites with a longevity of 100 years or more, there is, according to to the highly detailed and indisputable evidence, no evidence of global warming, or its resultant: climate change, in Australia.

26d) That being the case Greta has admitted and agreed as per section 17.3 of the NSW Uniform Civil Procedure Court Rules, the UCPR, that Australia has no case to answer and no cause to be bound by any accord or arrangement.

26e) This renders a massive boost, our booster shot, to our national economy that Australia is not saddled with needless punative climate change payments to be made to elites overseas. Thank you Greta for your very considered December 25th Christmas present!

26f) In arriving at her admissions, Greta and the IPCC had access to all the data and could find no fault with it and so released Australia from any binding obligations pursuant to sections 17.3 and 17.7 of the UCPR, (click on links), which findings are upliftable to any court of law in the world.

26g) Now with Greta’s and the IPCC’s considered and binding Australia admissions no one need pay heed to any carbon credit requirements and all such moneys paid can be claimed and clawed back of the parties who collected them off you as those parties can now claim any remitted moneys back pursuant to Greta and the IPCC’s studiously considered admissions under pain of bankruptcy.

26h) Six Section 17.3 Admission Attachments in Chronological Order

n2af_to_Climate_Action_BCB_and_Ms_Fiona_Martin_MLA.mbox

n2af_to_Climate_Action_BCB_and_Ms_Fiona_Martin_MP_and_Matt_Kean.mbox

27) *** For those interested in the common law alternative to unstructured, and hence uncommitted, somewhat dicey legal institution of marriage, being the common law Relationship Agreement legal alternative where assets are not at risk and creative commitment is proven. A committed to, operating Relationship Agreement gives structure, purpose and direction to any serious marriage or relationship and should be put in place by each partner in honour of each other. To obtain your binding copy please click here.

28) *** To learn how to manage your money and your savings, in the way I have learned to do since I was 14, so that you can be financially and debt free, please go to my website devfinresp.org

AUDIOS:

29) Here is a link to our latest up to date talk given on 23.1.2022

30) Click here for Audio of Meeting with Pamela on 29.10.21 on how to get started after viewing Aussiedebtbailout.org, (37 min).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

SPECIAL AND UNUSUAL OFFER

33) As a doctor I currently have some 50 very valuable negotiable promissory note type invited invoices that a corruptly run contemptible NSW government department, which is populated (“two thirds” majority) by contracted obsolete moribund dinosaurs and defiantly in MHA sections 68e, CCA 4+45 breach, and has got themselves in the pooh and has made comprehensive section 17.3 admissions whilst working hard over 35 years faking a fictitious defence to fool the court, has invited me to serve on them from February 2020 to December 2021 so that they could make donations of money. The said government department keeps inviting me to serve these ever increasing invoices fortnightly as it is the cheaper of three options available to them rather than admitting they have no defence.

34) The negotiable invoices range in face value from $200,000 to $3,900,000. I am happy to let any of them go for only 15% of their face value (i.e $30,000 to $585,000). With the assistance of a good solicitor or accountant you, or a friend, can use the higher value ones to buy a property etc for effectively only 15% of a vendor’s asking price by using them as legal tender currency to settle a purchase. Please contact me if you would like to acquire one or more of these invited invoices for only 15% face value.

35) Click here for a summary of 16 life improvement options for those who might be interested in some more items.

36) ‘Prof’ St Dr David G Murphy

Investor by an Order of the Supreme Court, Funds Owner and Law Therapist, CCP Lienor and Liquidator: Lieniquidator.

Scion and Heir Successor to the Revolution

Asherah Magdalene Common Law Reserves Temple Charitybank

Chairperson STAAG, Sydney Treatment Alternatives Advocacy Group,

CEO Midwest Research (SCWL) Australasia

Sydney, Australia

(+61) 419 605 365, 0419 605 365

Click here to email this webpage to friends etc.